China’s economic slowdown already being felt throughout world economy

Vincent Kolo, chinaworker.info

“The most important number in the world, for the past 30 years and next five years, is China’s growth rate,” declared BBC Economics Editor Robert Peston. With a stream of data confirming a pronounced slowdown in the Chinese economy, fears are rising that this will act as a drag rather than a motor for global capitalism. China’s housing market, which has been the main locomotive of growth for the past decade, is faltering, as is business investment and factory output. The Chinese regime is not only navigating the slowest GDP growth for a quarter century, but simultaneously trying to speed up neo-liberal restructuring in order to spur private investment and domestic consumption. This is part of its strategy to wean the economy off its addiction to debt, now running at over 250 percent of GDP, an exceptionally high level for a developing economy.

Many commentators now expect this year’s GDP to fall short of the government’s 7.5 target, something that hasn’t happened for sixteen years. Even the target figure represents China’s slowest annual growth since 1990. Following the top CCP leadership’s Central Economic Work Conference in mid-December, which declared “downward pressure on China’s economy is relatively big”, it is widely anticipated that the 2015 GDP target will be further lowered to 7 percent.

The term “new normal” to underline lower GDP growth has been adopted by the CCP regime and widely promoted in the state media. Xi Jinping claims to have developed the “new normal” as a theory – while in fact this term has been plagiarized from Western media descriptions of the post-2008 global crisis. “The ‘new normal’ theory elaborated by Chinese President Xi Jinping would be one of the hallmarks to be engraved in history,” trumpeted the Global Times. The regime is trying to pull the wool over people’s eyes by presenting the deepening slowdown as a deliberate and intended policy, as something positive. While it is true that the neo-liberal reformers advocate slower “quality” growth (by which they mean less state control and a reduction of debt-funded investment), there are myriad factors at work in the economy today that Beijing does not control and which could set-off economic shockwaves in the coming period.

China number one?

According to a recent and hotly debated report from the International Monetary Fund (IMF), China is now the world’s largest economy. If correct, this marks the end of 142 years of US pre-eminence dating back to when Ulysses S. Grant was president. Measured by purchasing power parities (a method using local rather than global prices) China’s economy is now worth US$17.6 trillion compared to US GDP of US$17.4 trillion. By the end of the decade the Chinese economy will be 20 percent bigger than the US, says the IMF. While the jury is still out on whether this global economic shift has already occurred, due to different methodology, few commentators doubt that it will occur in the years ahead. Hence also the increased concerns as China’s economy encounters growing difficulties, which go much deeper than falling GDP growth rates.

According to a recent and hotly debated report from the International Monetary Fund (IMF), China is now the world’s largest economy. If correct, this marks the end of 142 years of US pre-eminence dating back to when Ulysses S. Grant was president. Measured by purchasing power parities (a method using local rather than global prices) China’s economy is now worth US$17.6 trillion compared to US GDP of US$17.4 trillion. By the end of the decade the Chinese economy will be 20 percent bigger than the US, says the IMF. While the jury is still out on whether this global economic shift has already occurred, due to different methodology, few commentators doubt that it will occur in the years ahead. Hence also the increased concerns as China’s economy encounters growing difficulties, which go much deeper than falling GDP growth rates.

The current turmoil in global commodity markets, most notably with the collapse in oil prices, is a result of global supply outstripping demand – something we also see graphically in the number one market, China. Several factors are behind this, not least the “shale revolution” which has boosted US oil and gas production. China is suffering historically unprecedented levels of overcapacity for everything from steel to solar panels and nowhere is this more glaring than in the housing market. House sales nationally fell by 10 percent in 2014 and the country now has around seven years worth of unsold housing inventory, according to real estate expert Ai Jingwei. A Beijing business newspaper has published a “ghost town index” stating there are at least 50 cities in which half or more of the housing is unoccupied.

China’s construction sector consumes around half the world’s steel and cement and employs 37 million people – which is 23 percent more than the entire working population of Britain. The past decade’s building boom has therefore also been a huge driver of global energy prices, with China accounting for more than half the world’s construction activity, and construction consuming almost one-third of global energy usage.

Commodity markets reeling

By December, the commodities downturn was the main trigger of sharp falls on global stock markets; with the Shanghai market also experiencing its biggest one-day drop (5 percent) since 2009. The slump in commodity markets has led many economic commentators to again question if China’s official GDP figures reflect the real picture. As Bloomberg columnist William Pesek commented, “For anyone who thinks China is operating even close to that number [i.e. 7.5 percent growth], I have two words: iron ore. Even more than the plunge in oil, the halving of prices for these pivotal rocks and minerals – as well as a 44 per cent dive in oil and tumble in coal and other commodities – suggests China may be braking rapidly.”

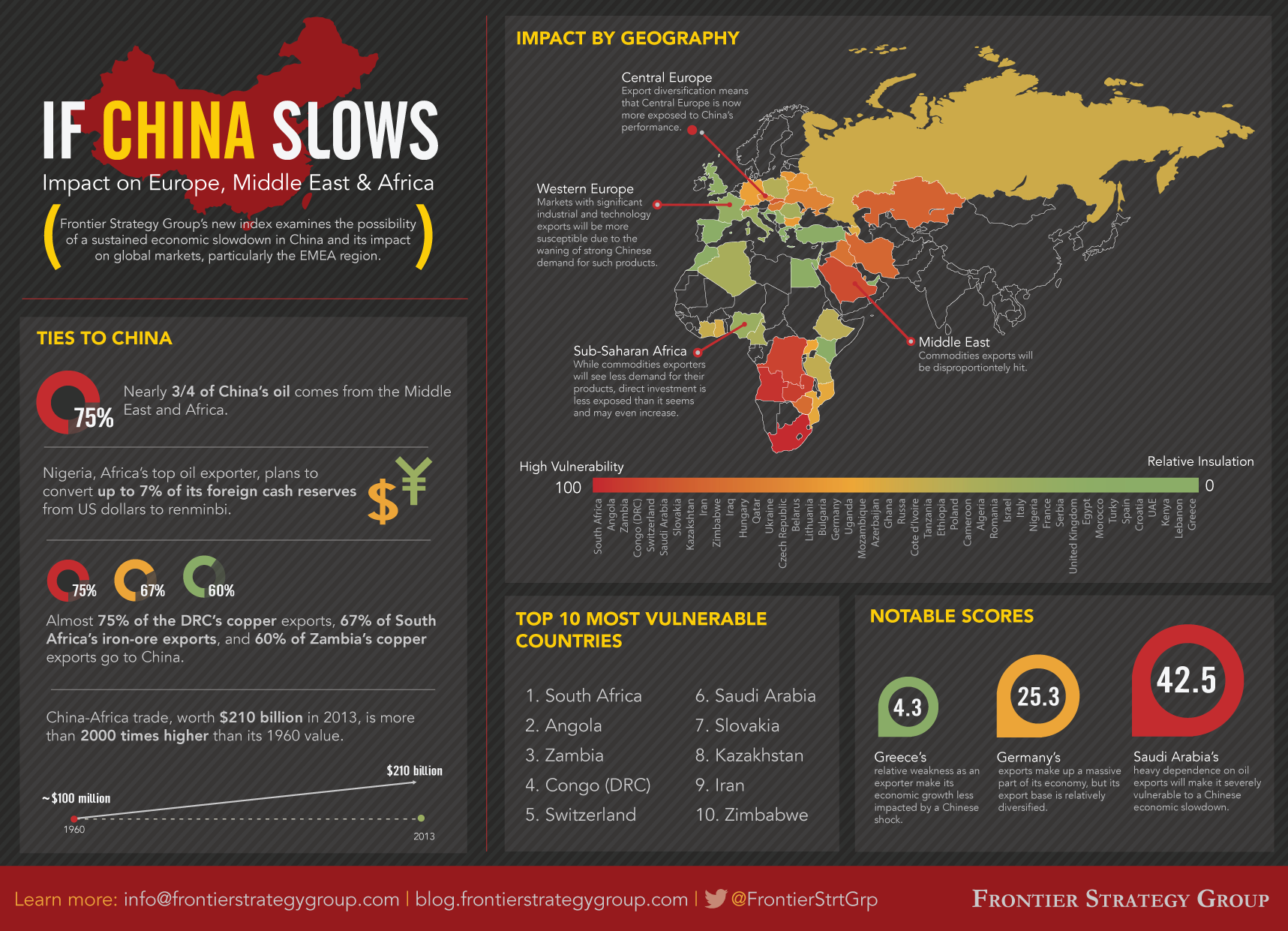

Falling commodity prices have pushed many commodity exporters into recession and balance of payments crises. Oil-dependent Venezuela, having slipped into recession, may be forced to default on its international loans, which are mainly to Chinese state banks. There is speculation that the government of Nicolás Maduro will seek an extension of credit lines from Beijing, effectively a bailout. “The Chinese are shrewd and they may want [oil] fields in the Orinoco region in return for whatever aid package China develops,” one commentator told China Daily. Even Russia, in the grip of a currency crisis (the ruble lost half its value in 2014) and squeezed by collapsing oil revenues and Western sanctions, may be forced to turn to China for financial help.

The government of Zambia, whose copper mines are mostly Chinese-owned, has been forced to call in the vampires of the IMF to ‘rescue’ its finances – which translates into new austerity measures for the Zambian people. Even ‘the lucky country’ Australia, which until now has largely escaped the global crisis thanks to its burgeoning China trade, reported the biggest drop since 1960 in its terms of trade (falling export revenues while import costs rise). Like poorer commodity exporters Australia has ridden on the China construction boom, with huge gains for its mining companies, but at the cost of a further decline in its domestic manufacturing base. Today, however, a quarter of Australia’s thermal coalmines are unprofitable, according to Glencore. The commodities shakeout linked to China’s slowdown means tough times for these countries and points to China exercising greater control – in a more openly imperialist manner – over markets and governments that are dependent on its financial power.

Overcapacity

Chinese steel capacity has expanded furiously, driven by frenzied and increasingly speculative investment in property and infrastructure construction. This expansion has continued despite already absurd levels of overcapacity, which the Chinese regime has now pledged to rein in, although achieving this is no straightforward matter. Similar over-investment has occurred in cement, glass, coal mining, aluminium, shipbuilding and a plethora of other industries, backed by an unprecedented credit explosion – an additional US$19 trillion since the onset of the global capitalist crisis in 2008.

A report in November by two government economists estimates that up to half of all investment over the past five years, 42 trillion yuan worth, has been wasted (Xu Ce of the National Development and Reform Commission, and Wang Yuan of the Academy of Macro Economic Research). The problem has worsened, they say, over the past two years i.e. since Xi came to power.

China’s steel output is now seven times greater than that of Japan, the world’s number two steel producer. Idle capacity alone is more than twice the size of the US steel industry. Overproduction has led to a price war with steel prices in some regions of China falling as low as the price of cabbage. In 2012, China had the capacity to produce 2.9 billion tons of cement, but actual demand was only for 2.1 billion tons. Three quarters of China’s 200 biggest airports are losing money, but there are plans to build 100 more.

A similar pattern has been repeated in industry after industry as cities and regions attempt to outstrip each other with little consideration for the overall state of the national economy. The result has been an extremely rapid accumulation of debt by companies and local governments that threatens a wave of corporate failures and a banking crisis, as the market is flooded, profits are squeezed, and credit costs shoot upwards.

Beijing’s difficulties are magnified by the growth of the shadow banking sector – now the world’s third largest – which serves as an unofficial channel for the state-owned banks to circumvent government regulation in order to maintain the flow of credit to distressed corporate borrowers.

Inevitably the working class is paying the price for the ill planned and in many cases purely speculative investment of the past period. One indication is the upturn in strikes in the construction sector – 55 strikes from July to September. This industry is notorious for its multiple layers of sub contractors that rely on uninsured, unprotected and low-paid migrant workers. A report from Hong Kong-based China Labour Bulletin noted that with a rise in de facto defaults and the suspension of many projects, “construction workers are always the last to be paid.” Half of all strikes in China in the latter part of 2014 were linked to wage arrears.

The situation in the coal industry is even worse. 70 percent of China’s coalmines are running at a loss through a combination of falling global coal prices (down 25 percent in 2014), excess capacity, and the government’s anti-pollution measures. More than half of coalmines are struggling to pay their employees’ wages, according to the chairman of the China Coal Industry Association, Wang Xianzheng. Consequently, major coal producing regions such as Shanxi province are on the frontline as concerns rise over financial stress, with reports of imminent shadow banking defaults.

The scourge of deflation

When China’s central bank, in a surprise move, cut its benchmark interest rates on November 21, this was a signal that economic ‘fundamentals’ are considerably worse than the government would have us believe. The fear of deflation is clearly now uppermost as the regime shifts towards what will likely be further monetary loosening measures in the course of 2015. The official consumer inflation figure for November was 1.4 percent, the lowest for five years. But prices at the factory gate fell 2.7 percent (November year-on-year) and this marks 33 months of consecutive price falls. As the Economist magazine noted, China “is now skirting close to outright falls in prices across a wide swathe of the economy.”

Deflation arises when financial bubbles burst as occurred in Japan when its property bubble collapsed in the early 1990s, and today in China as a result of overproduction and over-construction. When widespread across an entire economy, falling prices depress economic growth as consumers put off buying goods and companies delay investments. Worst of all, deflation exacerbates the debt burden for companies and governments by increasing the real cost of loans.

Debt service charges have reached 17 percent of China’s GDP, according to the Financial Times, an increase from 7.5 percent of GDP in 2011. The central bank’s move to cut interest rates, probably to be followed by increases in the capital base of the banks (by cutting the required reserve ratio), is mainly intended to ease the debt servicing costs of China’s companies and local governments as a wave of defaults looms. This is already happening, but has been disguised by shuffling bad debts from one entity to another within the banking system. Due to the effects of falling inflation the real cost of borrowing has soared from zero to 5 percent since 2011.

However, the most immediate effect of November’s interest rate cut was to inflate a new stock market bubble, with the Shanghai Composite Index surging more than 25 percent in four weeks. Much of this influx has been through so-called ‘margin trading’ – only legalized in China in 2012 – a highly risky practice whereby speculators use borrowed cash rather than their own capital to trade in stocks. A veritable gold rush has occurred with hundreds of thousands of new trading accounts opened in recent weeks while banks have also rushed to roll out new lending platforms to feed the ‘margin trading’ fever. Thus Beijing faces an acute dilemma in that its anti-deflationary measures risk triggering new financial bubbles and exacerbating the debt crisis.

The risk of a deflationary spiral is now the major worry for Xi and his economic team, and for the capitalist class worldwide, as shown by the similar policies of the European and Japanese central banks: to create inflation by “any means necessary”. Whether China’s economy will suffer a hard landing in the next period (commonly defined as GDP growth below 5 percent) is an open question. Some economists warn that a “long landing” is the most likely scenario, echoing our own predictions that China is now entering a ‘Japanese phase’ of deflation, debt crisis and stagnation, with major implications for the class struggle and political stability in the period ahead.